Fully annotated reference manual - version 1.8.13.0

Loading...

Searching...

No Matches

Commodity Swaption Analytical Engine. More...

#include <qle/pricingengines/commodityswaptionengine.hpp>

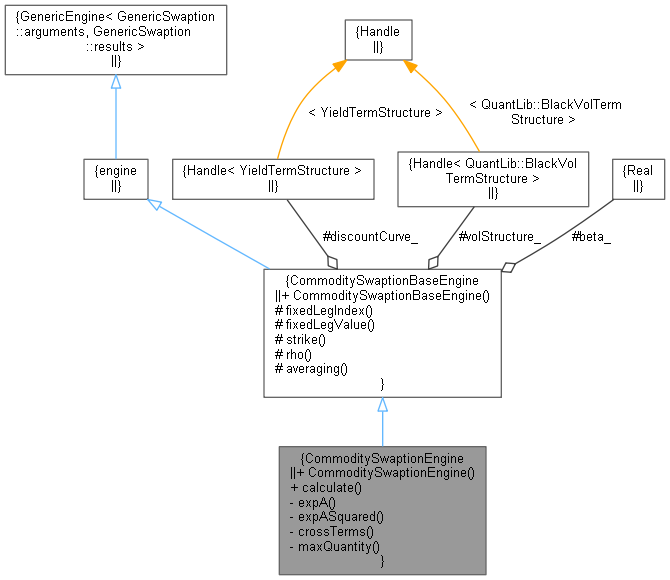

Inheritance diagram for CommoditySwaptionEngine: Collaboration diagram for CommoditySwaptionEngine:

Inheritance diagram for CommoditySwaptionEngine: Collaboration diagram for CommoditySwaptionEngine:Public Member Functions | |

| CommoditySwaptionEngine (const Handle< YieldTermStructure > &discountCurve, const Handle< QuantLib::BlackVolTermStructure > &vol, Real beta=0.0) | |

| void | calculate () const override |

| Public Member Functions inherited from CommoditySwaptionBaseEngine | |

| CommoditySwaptionBaseEngine (const Handle< YieldTermStructure > &discountCurve, const Handle< QuantLib::BlackVolTermStructure > &vol, Real beta=0.0) | |

Private Member Functions | |

| QuantLib::Real | expA (QuantLib::Size floatLegIndex, QuantLib::Real normFactor) const |

| QuantLib::Real | expASquared (QuantLib::Size floatLegIndex, QuantLib::Real strike, QuantLib::Real normFactor) const |

| QuantLib::Real | crossTerms (const QuantLib::ext::shared_ptr< QuantLib::CashFlow > &cf_1, const QuantLib::ext::shared_ptr< QuantLib::CashFlow > &cf_2, bool isAveraging, QuantLib::Real strike, QuantLib::Real normFactor) const |

| QuantLib::Real | maxQuantity (QuantLib::Size floatLegIndex) const |

Additional Inherited Members | |

| Protected Member Functions inherited from CommoditySwaptionBaseEngine | |

| QuantLib::Size | fixedLegIndex () const |

| QuantLib::Real | fixedLegValue (QuantLib::Size fixedLegIndex) const |

| Give back the fixed leg price at the swaption expiry time. More... | |

| QuantLib::Real | strike (QuantLib::Size fixedLegIndex) const |

| QuantLib::Real | rho (const QuantLib::Date &ed_1, const QuantLib::Date &ed_2) const |

| bool | averaging (QuantLib::Size floatLegIndex) const |

| Protected Attributes inherited from CommoditySwaptionBaseEngine | |

| Handle< YieldTermStructure > | discountCurve_ |

| Handle< QuantLib::BlackVolTermStructure > | volStructure_ |

| Real | beta_ |

Commodity Swaption Analytical Engine.

Analytical pricing based on the two-moment Turnbull-Wakeman approximation similar to APO pricing. Reference: Iain Clark, Commodity Option Pricing, Wiley, section 2.8 See also the documentation in the ORE+ product catalogue.

Definition at line 79 of file commodityswaptionengine.hpp.

| CommoditySwaptionEngine | ( | const Handle< YieldTermStructure > & | discountCurve, |

| const Handle< QuantLib::BlackVolTermStructure > & | vol, | ||

| Real | beta = 0.0 |

||

| ) |

Definition at line 81 of file commodityswaptionengine.hpp.

|

override |

Definition at line 167 of file commodityswaptionengine.cpp.

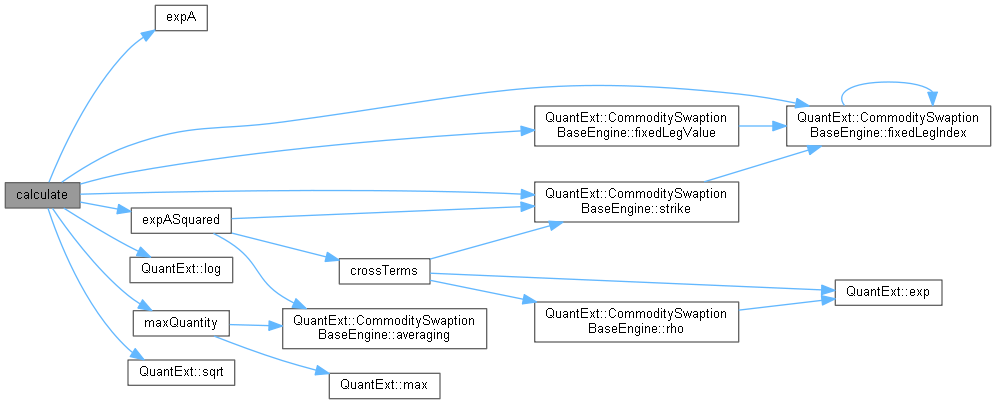

Here is the call graph for this function:

|

private |

Calculate the expected value of the floating leg at the swaption expiry date i.e. the expected value of the quantity A(t_e) from the ORE+ Product Catalogue. Quantities in the calculation are divided by the normFactor to guard against numerical blow up.

Definition at line 219 of file commodityswaptionengine.cpp.

Here is the caller graph for this function:

|

private |

Calculate the expected value of the floating leg squared at the swaption expiry date i.e. the expected value of the quantity A^2(t_e) from the ORE+ Product Catalogue. Quantities in the calculation are divided by the normFactor to guard against numerical blow up.

Definition at line 235 of file commodityswaptionengine.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

|

private |

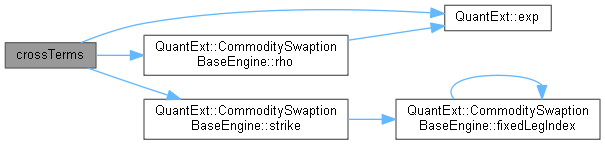

Calculate the cross terms involved in expASquared. Quantities in the calculation are divided by the normFactor to guard against numerical blow up.

Definition at line 261 of file commodityswaptionengine.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

|

private |

Return the maximum quantity over all cashflows on the commodity floating leg. This is used as a normalisation factor in the calculation of E[A(t_e)] and E[A^2(t_e)] to guard against blow up.

Definition at line 401 of file commodityswaptionengine.cpp.

Here is the call graph for this function: Here is the caller graph for this function: