Fully annotated reference manual - version 1.8.13.0

Loading...

Searching...

No Matches

Commodity Basis Future Index. More...

#include <qle/indexes/commoditybasisfutureindex.hpp>

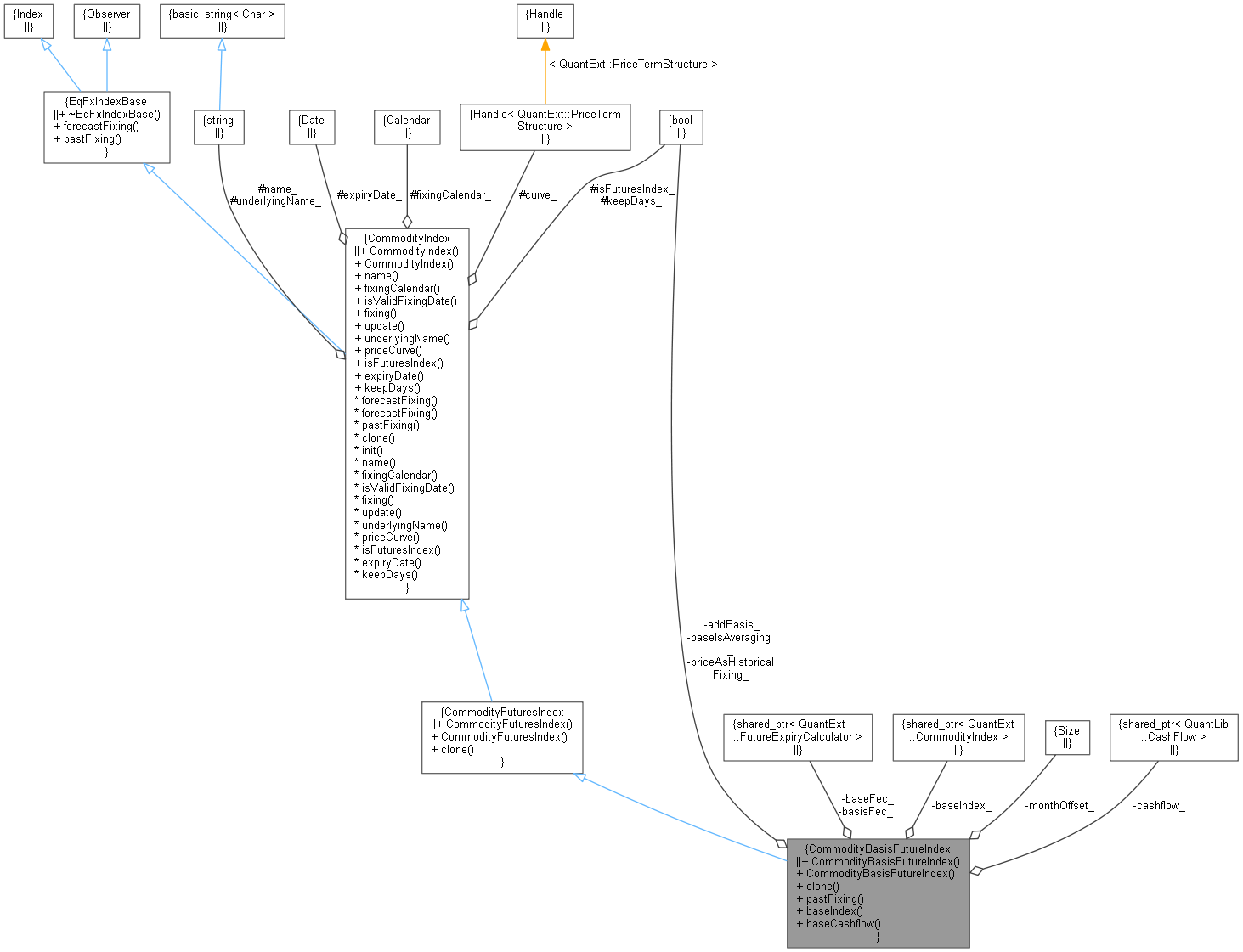

Inheritance diagram for CommodityBasisFutureIndex: Collaboration diagram for CommodityBasisFutureIndex:

Inheritance diagram for CommodityBasisFutureIndex: Collaboration diagram for CommodityBasisFutureIndex:Public Member Functions | |

| CommodityBasisFutureIndex (const std::string &underlyingName, const QuantLib::Date &expiryDate, const QuantLib::Calendar &fixingCalendar, const QuantLib::ext::shared_ptr< FutureExpiryCalculator > &basisFec, const QuantLib::ext::shared_ptr< QuantExt::CommodityIndex > &baseIndex, const QuantLib::ext::shared_ptr< FutureExpiryCalculator > &baseFec, const QuantLib::Handle< QuantExt::PriceTermStructure > &priceCurve=QuantLib::Handle< QuantExt::PriceTermStructure >(), const bool addBasis=true, const QuantLib::Size monthOffset=0, const bool baseIsAveraging=false, const bool priceAsHistoricalFixing=true) | |

| CommodityBasisFutureIndex (const std::string &underlyingName, const QuantLib::Date &expiryDate, const QuantLib::Calendar &fixingCalendar, const QuantLib::ext::shared_ptr< CommodityBasisPriceTermStructure > &priceCurve) | |

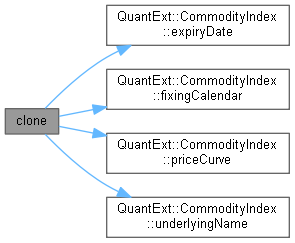

| QuantLib::ext::shared_ptr< CommodityIndex > | clone (const QuantLib::Date &expiryDate=QuantLib::Date(), const boost::optional< QuantLib::Handle< PriceTermStructure > > &ts=boost::none) const override |

| Implement the base clone. Ajust the base future to match the same contract month. More... | |

| QuantLib::Real | pastFixing (const QuantLib::Date &fixingDate) const override |

| const QuantLib::ext::shared_ptr< QuantExt::CommodityIndex > & | baseIndex () |

| QuantLib::ext::shared_ptr< QuantLib::CashFlow > | baseCashflow (const QuantLib::Date &paymentDate=QuantLib::Date()) const |

| Public Member Functions inherited from CommodityFuturesIndex | |

| CommodityFuturesIndex (const std::string &underlyingName, const Date &expiryDate, const Calendar &fixingCalendar, const Handle< QuantExt::PriceTermStructure > &priceCurve=Handle< QuantExt::PriceTermStructure >()) | |

| CommodityFuturesIndex (const std::string &underlyingName, const Date &expiryDate, const Calendar &fixingCalendar, bool keepDays, const Handle< QuantExt::PriceTermStructure > &priceCurve=Handle< QuantExt::PriceTermStructure >()) | |

| QuantLib::ext::shared_ptr< CommodityIndex > | clone (const QuantLib::Date &expiryDate=QuantLib::Date(), const boost::optional< QuantLib::Handle< PriceTermStructure > > &ts=boost::none) const override |

| Implement the base clone. More... | |

| Public Member Functions inherited from CommodityIndex | |

| CommodityIndex (const std::string &underlyingName, const QuantLib::Date &expiryDate, const Calendar &fixingCalendar, const Handle< QuantExt::PriceTermStructure > &priceCurve=Handle< QuantExt::PriceTermStructure >()) | |

| CommodityIndex (const std::string &underlyingName, const QuantLib::Date &expiryDate, const Calendar &fixingCalendar, bool keepDays, const Handle< QuantExt::PriceTermStructure > &priceCurve=Handle< QuantExt::PriceTermStructure >()) | |

| std::string | name () const override |

| Calendar | fixingCalendar () const override |

| bool | isValidFixingDate (const Date &fixingDate) const override |

| Real | fixing (const Date &fixingDate, bool forecastTodaysFixing=false) const override |

| void | update () override |

| std::string | underlyingName () const |

| const Handle< QuantExt::PriceTermStructure > & | priceCurve () const |

| bool | isFuturesIndex () const |

| const QuantLib::Date & | expiryDate () const |

| bool | keepDays () const |

| virtual Real | forecastFixing (const Date &fixingDate) const |

| virtual Real | forecastFixing (const Time &fixingTime) const override |

| returns the fixing at the given time More... | |

| virtual Real | pastFixing (const Date &fixingDate) const override |

| returns a past fixing at the given date More... | |

| Public Member Functions inherited from EqFxIndexBase | |

| virtual | ~EqFxIndexBase () |

| virtual Real | forecastFixing (const Time &fixingTime) const =0 |

| returns the fixing at the given time More... | |

| virtual Real | pastFixing (const Date &fixingDate) const =0 |

| returns a past fixing at the given date More... | |

Private Attributes | |

| QuantLib::ext::shared_ptr< FutureExpiryCalculator > | basisFec_ |

| QuantLib::ext::shared_ptr< QuantExt::CommodityIndex > | baseIndex_ |

| QuantLib::ext::shared_ptr< FutureExpiryCalculator > | baseFec_ |

| bool | addBasis_ |

| QuantLib::Size | monthOffset_ |

| bool | baseIsAveraging_ |

| bool | priceAsHistoricalFixing_ |

| QuantLib::ext::shared_ptr< QuantLib::CashFlow > | cashflow_ |

Additional Inherited Members | |

| Protected Member Functions inherited from CommodityIndex | |

| void | init () |

| Protected Attributes inherited from CommodityIndex | |

| std::string | underlyingName_ |

| Date | expiryDate_ |

| Calendar | fixingCalendar_ |

| Handle< QuantExt::PriceTermStructure > | curve_ |

| std::string | name_ |

| bool | isFuturesIndex_ |

| bool | keepDays_ |

Commodity Basis Future Index.

This index can represent futures prices derived from basis future index and a base future index

Definition at line 36 of file commoditybasisfutureindex.hpp.

| CommodityBasisFutureIndex | ( | const std::string & | underlyingName, |

| const QuantLib::Date & | expiryDate, | ||

| const QuantLib::Calendar & | fixingCalendar, | ||

| const QuantLib::ext::shared_ptr< FutureExpiryCalculator > & | basisFec, | ||

| const QuantLib::ext::shared_ptr< QuantExt::CommodityIndex > & | baseIndex, | ||

| const QuantLib::ext::shared_ptr< FutureExpiryCalculator > & | baseFec, | ||

| const QuantLib::Handle< QuantExt::PriceTermStructure > & | priceCurve = QuantLib::Handle<QuantExt::PriceTermStructure>(), |

||

| const bool | addBasis = true, |

||

| const QuantLib::Size | monthOffset = 0, |

||

| const bool | baseIsAveraging = false, |

||

| const bool | priceAsHistoricalFixing = true |

||

| ) |

Definition at line 22 of file commoditybasisfutureindex.cpp.

Here is the call graph for this function:| CommodityBasisFutureIndex | ( | const std::string & | underlyingName, |

| const QuantLib::Date & | expiryDate, | ||

| const QuantLib::Calendar & | fixingCalendar, | ||

| const QuantLib::ext::shared_ptr< CommodityBasisPriceTermStructure > & | priceCurve | ||

| ) |

Definition at line 45 of file commoditybasisfutureindex.cpp.

|

overridevirtual |

Implement the base clone. Ajust the base future to match the same contract month.

Implements CommodityIndex.

Definition at line 55 of file commoditybasisfutureindex.cpp.

Here is the call graph for this function:

|

override |

Definition at line 76 of file commoditybasisfutureindex.cpp.

Here is the call graph for this function:| const QuantLib::ext::shared_ptr< QuantExt::CommodityIndex > & baseIndex | ( | ) |

Definition at line 59 of file commoditybasisfutureindex.hpp.

Here is the caller graph for this function:| QuantLib::ext::shared_ptr< QuantLib::CashFlow > baseCashflow | ( | const QuantLib::Date & | paymentDate = QuantLib::Date() | ) | const |

Definition at line 64 of file commoditybasisfutureindex.cpp.

Here is the call graph for this function: Here is the caller graph for this function:

|

private |

Definition at line 63 of file commoditybasisfutureindex.hpp.

|

private |

Definition at line 64 of file commoditybasisfutureindex.hpp.

|

private |

Definition at line 65 of file commoditybasisfutureindex.hpp.

|

private |

Definition at line 66 of file commoditybasisfutureindex.hpp.

|

private |

Definition at line 67 of file commoditybasisfutureindex.hpp.

|

private |

Definition at line 68 of file commoditybasisfutureindex.hpp.

|

private |

Definition at line 69 of file commoditybasisfutureindex.hpp.

|

private |

Definition at line 70 of file commoditybasisfutureindex.hpp.