Fully annotated reference manual - version 1.8.13.0

Loading...

Searching...

No Matches

ScenarioSimMarket description. More...

#include <orea/scenario/scenariosimmarketparameters.hpp>

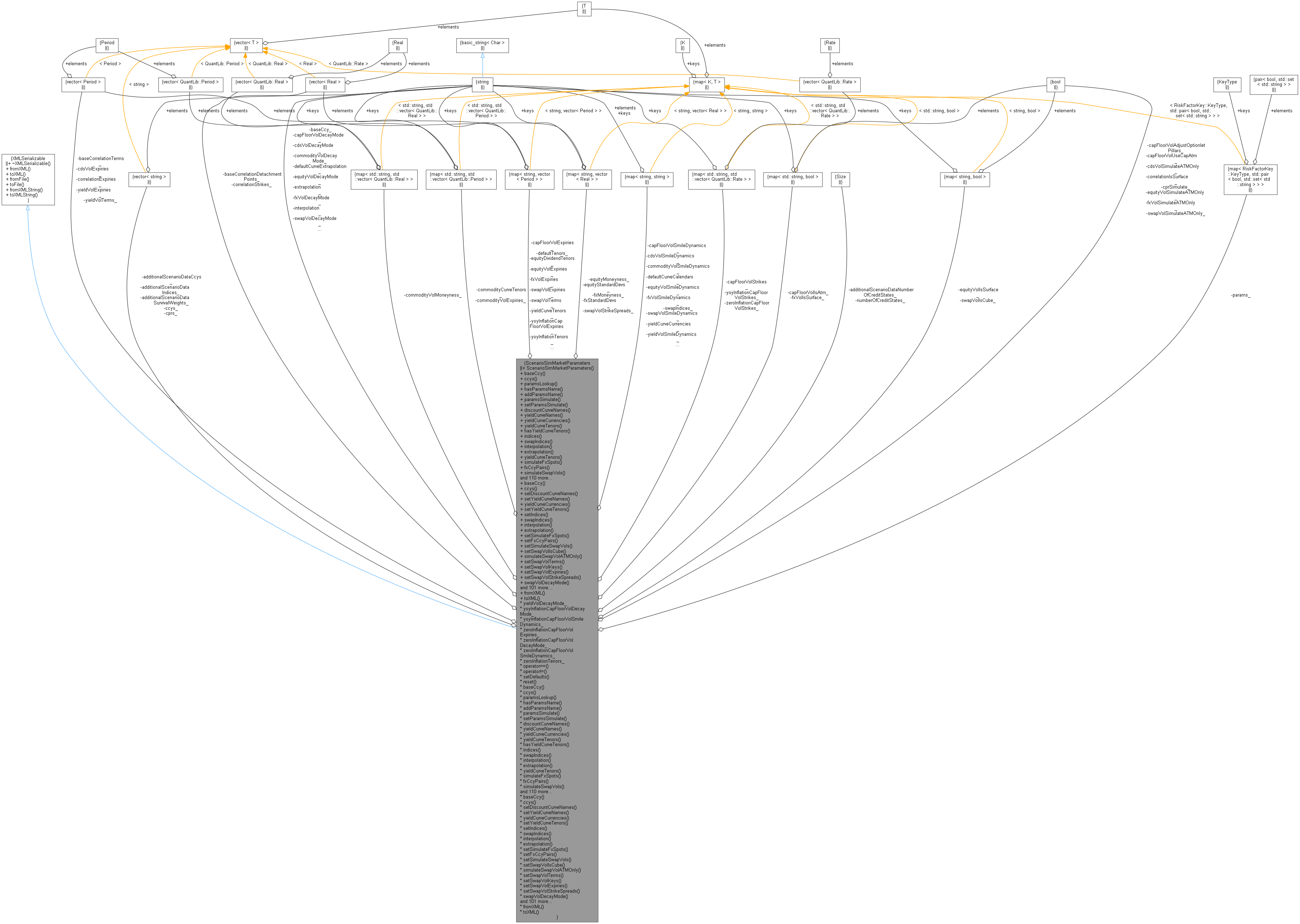

Inheritance diagram for ScenarioSimMarketParameters: Collaboration diagram for ScenarioSimMarketParameters:

Inheritance diagram for ScenarioSimMarketParameters: Collaboration diagram for ScenarioSimMarketParameters:Public Member Functions | |

| ScenarioSimMarketParameters () | |

| Default constructor. More... | |

Inspectors | |

| const string & | baseCcy () const |

| const vector< string > & | ccys () const |

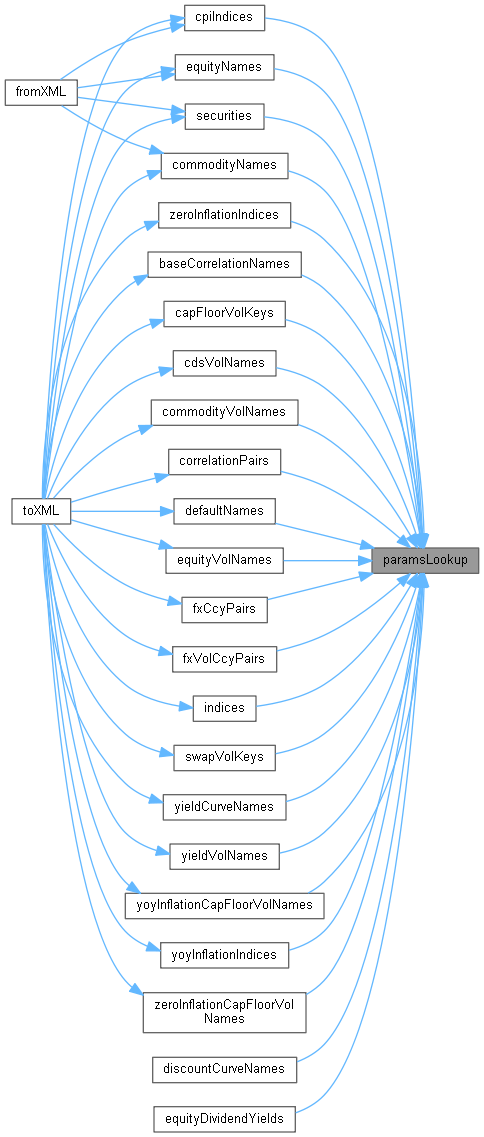

| vector< string > | paramsLookup (RiskFactorKey::KeyType k) const |

| bool | hasParamsName (RiskFactorKey::KeyType kt, string name) const |

| void | addParamsName (RiskFactorKey::KeyType kt, vector< string > names) |

| bool | paramsSimulate (RiskFactorKey::KeyType kt) const |

| void | setParamsSimulate (RiskFactorKey::KeyType kt, bool simulate) |

| vector< string > | discountCurveNames () const |

| vector< string > | yieldCurveNames () const |

| const map< string, string > & | yieldCurveCurrencies () const |

| const vector< Period > & | yieldCurveTenors (const string &key) const |

| bool | hasYieldCurveTenors (const string &key) const |

| vector< string > | indices () const |

| const map< string, string > & | swapIndices () const |

| const string & | interpolation () const |

| const string & | extrapolation () const |

| const map< string, vector< Period > > & | yieldCurveTenors () const |

| bool | simulateFxSpots () const |

| vector< string > | fxCcyPairs () const |

| bool | simulateSwapVols () const |

| bool | swapVolIsCube (const string &key) const |

| bool | simulateSwapVolATMOnly () const |

| const vector< Period > & | swapVolTerms (const string &key) const |

| const vector< Period > & | swapVolExpiries (const string &key) const |

| vector< string > | swapVolKeys () const |

| const string & | swapVolDecayMode () const |

| const vector< Real > & | swapVolStrikeSpreads (const string &key) const |

| const string & | swapVolSmileDynamics (const string &key) const |

| bool | simulateYieldVols () const |

| const vector< Period > & | yieldVolTerms () const |

| const vector< Period > & | yieldVolExpiries () const |

| vector< string > | yieldVolNames () const |

| const string & | yieldVolDecayMode () const |

| const string & | yieldVolSmileDynamics (const string &key) const |

| bool | simulateCapFloorVols () const |

| vector< string > | capFloorVolKeys () const |

| const vector< Period > & | capFloorVolExpiries (const string &key) const |

| bool | hasCapFloorVolExpiries (const string &key) const |

| const vector< QuantLib::Rate > & | capFloorVolStrikes (const std::string &key) const |

| bool | capFloorVolIsAtm (const std::string &key) const |

| const string & | capFloorVolDecayMode () const |

| bool | capFloorVolAdjustOptionletPillars () const |

| bool | capFloorVolUseCapAtm () const |

| const string & | capFloorVolSmileDynamics (const string &key) const |

| bool | simulateYoYInflationCapFloorVols () const |

| vector< string > | yoyInflationCapFloorVolNames () const |

| const vector< Period > & | yoyInflationCapFloorVolExpiries (const string &key) const |

| bool | hasYoYInflationCapFloorVolExpiries (const string &key) const |

| const vector< Real > & | yoyInflationCapFloorVolStrikes (const std::string &key) const |

| const string & | yoyInflationCapFloorVolDecayMode () const |

| const string & | yoyInflationCapFloorVolSmileDynamics (const string &key) const |

| bool | simulateZeroInflationCapFloorVols () const |

| vector< string > | zeroInflationCapFloorVolNames () const |

| const vector< Period > & | zeroInflationCapFloorVolExpiries (const string &key) const |

| bool | hasZeroInflationCapFloorVolExpiries (const string &key) const |

| const vector< Real > & | zeroInflationCapFloorVolStrikes (const string &key) const |

| const string & | zeroInflationCapFloorVolDecayMode () const |

| const string & | zeroInflationCapFloorVolSmileDynamics (const string &key) const |

| bool | simulateSurvivalProbabilities () const |

| bool | simulateRecoveryRates () const |

| vector< string > | defaultNames () const |

| const string & | defaultCurveCalendar (const string &key) const |

| const vector< Period > & | defaultTenors (const string &key) const |

| bool | hasDefaultTenors (const string &key) const |

| const string & | defaultCurveExtrapolation () const |

| bool | simulateCdsVols () const |

| bool | simulateCdsVolATMOnly () const |

| const vector< Period > & | cdsVolExpiries () const |

| vector< string > | cdsVolNames () const |

| const string & | cdsVolDecayMode () const |

| const string & | cdsVolSmileDynamics (const string &key) const |

| vector< string > | equityNames () const |

| const vector< Period > & | equityDividendTenors (const string &key) const |

| bool | hasEquityDividendTenors (const string &key) const |

| vector< string > | equityDividendYields () const |

| bool | simulateDividendYield () const |

| bool | simulateFXVols () const |

| bool | simulateFxVolATMOnly () const |

| bool | fxVolIsSurface (const std::string &ccypair) const |

| bool | fxUseMoneyness (const std::string &ccypair) const |

| const vector< Period > & | fxVolExpiries (const string &key) const |

| const string & | fxVolDecayMode () const |

| vector< string > | fxVolCcyPairs () const |

| const vector< Real > & | fxVolMoneyness (const string &ccypair) const |

| const vector< Real > & | fxVolStdDevs (const string &ccypair) const |

| const string & | fxVolSmileDynamics (const string &key) const |

| bool | simulateEquityVols () const |

| bool | simulateEquityVolATMOnly () const |

| bool | equityUseMoneyness (const string &key) const |

| bool | equityVolIsSurface (const string &key) const |

| const vector< Period > & | equityVolExpiries (const string &key) const |

| const string & | equityVolDecayMode () const |

| vector< string > | equityVolNames () const |

| const vector< Real > & | equityVolMoneyness (const string &key) const |

| const vector< Real > & | equityVolStandardDevs (const string &key) const |

| const string & | equityVolSmileDynamics (const string &key) const |

| const vector< string > & | additionalScenarioDataIndices () const |

| const vector< string > & | additionalScenarioDataCcys () const |

| const Size | additionalScenarioDataNumberOfCreditStates () const |

| const vector< string > & | additionalScenarioDataSurvivalWeights () const |

| bool | securitySpreadsSimulate () const |

| vector< string > | securities () const |

| bool | simulateBaseCorrelations () const |

| const vector< Period > & | baseCorrelationTerms () const |

| const vector< Real > & | baseCorrelationDetachmentPoints () const |

| vector< string > | baseCorrelationNames () const |

| vector< string > | cpiIndices () const |

| vector< string > | zeroInflationIndices () const |

| const vector< Period > & | zeroInflationTenors (const string &key) const |

| bool | hasZeroInflationTenors (const string &key) const |

| vector< string > | yoyInflationIndices () const |

| const vector< Period > & | yoyInflationTenors (const string &key) const |

| bool | hasYoyInflationTenors (const string &key) const |

| bool | commodityCurveSimulate () const |

| std::vector< std::string > | commodityNames () const |

| const std::vector< QuantLib::Period > & | commodityCurveTenors (const std::string &commodityName) const |

| bool | hasCommodityCurveTenors (const std::string &commodityName) const |

| bool | commodityVolSimulate () const |

| const std::string & | commodityVolDecayMode () const |

| std::vector< std::string > | commodityVolNames () const |

| const std::vector< QuantLib::Period > & | commodityVolExpiries (const std::string &commodityName) const |

| const std::vector< QuantLib::Real > & | commodityVolMoneyness (const std::string &commodityName) const |

| const string & | commodityVolSmileDynamics (const string &commodityName) const |

| bool | simulateCorrelations () const |

| bool | correlationIsSurface () const |

| const vector< Period > & | correlationExpiries () const |

| vector< std::string > | correlationPairs () const |

| const vector< Real > & | correlationStrikes () const |

| Size | numberOfCreditStates () const |

| const std::map< RiskFactorKey::KeyType, std::pair< bool, std::set< std::string > > > & | parameters () const |

Setters | |

| string & | baseCcy () |

| vector< string > & | ccys () |

| void | setDiscountCurveNames (vector< string > names) |

| void | setYieldCurveNames (vector< string > names) |

| map< string, string > & | yieldCurveCurrencies () |

| void | setYieldCurveTenors (const string &key, const vector< Period > &p) |

| void | setIndices (vector< string > names) |

| map< string, string > & | swapIndices () |

| string & | interpolation () |

| string & | extrapolation () |

| void | setSimulateFxSpots (bool simulate) |

| void | setFxCcyPairs (vector< string > names) |

| void | setSimulateSwapVols (bool simulate) |

| void | setSwapVolIsCube (const string &key, bool isCube) |

| bool & | simulateSwapVolATMOnly () |

| void | setSwapVolTerms (const string &key, const vector< Period > &p) |

| void | setSwapVolKeys (vector< string > names) |

| void | setSwapVolExpiries (const string &key, const vector< Period > &p) |

| void | setSwapVolStrikeSpreads (const std::string &key, const std::vector< QuantLib::Rate > &strikes) |

| string & | swapVolDecayMode () |

| void | setSwapVolSmileDynamics (const string &key, const string &smileDynamics) |

| void | setSimulateYieldVols (bool simulate) |

| vector< Period > & | yieldVolTerms () |

| void | setYieldVolNames (vector< string > names) |

| vector< Period > & | yieldVolExpiries () |

| string & | yieldVolDecayMode () |

| void | setYieldVolSmileDynamics (const string &key, const string &smileDynamics) |

| void | setSimulateCapFloorVols (bool simulate) |

| void | setCapFloorVolKeys (vector< string > names) |

| void | setCapFloorVolExpiries (const string &key, const vector< Period > &p) |

| void | setCapFloorVolStrikes (const std::string &key, const std::vector< QuantLib::Rate > &strikes) |

| void | setCapFloorVolIsAtm (const std::string &key, bool isAtm) |

| string & | capFloorVolDecayMode () |

| void | setCapFloorVolAdjustOptionletPillars (bool capFloorVolAdjustOptionletPillars) |

| void | setCapFloorVolUseCapAtm (bool capFloorVolUseCapAtm) |

| void | setCapFloorVolSmileDynamics (const string &key, const string &smileDynamics) |

| void | setSimulateYoYInflationCapFloorVols (bool simulate) |

| void | setYoYInflationCapFloorVolNames (vector< string > names) |

| void | setYoYInflationCapFloorVolExpiries (const string &key, const vector< Period > &p) |

| void | setYoYInflationCapFloorVolStrikes (const std::string &key, const std::vector< QuantLib::Rate > &strikes) |

| string & | yoyInflationCapFloorVolDecayMode () |

| void | setYoYInflationCapFloorVolSmileDynamics (const string &key, const string &smileDynamics) |

| void | setSimulateZeroInflationCapFloorVols (bool simulate) |

| void | setZeroInflationCapFloorNames (vector< string > names) |

| void | setZeroInflationCapFloorVolExpiries (const string &key, const vector< Period > &p) |

| void | setZeroInflationCapFloorVolStrikes (const std::string &key, const std::vector< QuantLib::Rate > &strikes) |

| string & | zeroInflationCapFloorVolDecayMode () |

| void | setZeroInflationCapFloorVolSmileDynamics (const string &key, const string &smileDynamics) |

| void | setSimulateSurvivalProbabilities (bool simulate) |

| void | setSimulateRecoveryRates (bool simulate) |

| void | setDefaultNames (vector< string > names) |

| void | setDefaultTenors (const string &key, const vector< Period > &p) |

| void | setDefaultCurveCalendars (const string &key, const string &p) |

| void | setDefaultCurveExtrapolation (const std::string &e) |

| void | setSimulateCdsVols (bool simulate) |

| void | setSimulateCdsVolsATMOnly (bool simulateATMOnly) |

| vector< Period > & | cdsVolExpiries () |

| void | setCdsVolNames (vector< string > names) |

| string & | cdsVolDecayMode () |

| void | setCdsVolSmileDynamics (const string &key, const string &smileDynamics) |

| void | setEquityNames (vector< string > names) |

| void | setEquityDividendCurves (vector< string > names) |

| void | setEquityDividendTenors (const string &key, const vector< Period > &p) |

| void | setSimulateDividendYield (bool simulate) |

| void | setSimulateFXVols (bool simulate) |

| void | setSimulateFxVolATMOnly (bool simulateATMOnly) |

| void | setFxVolIsSurface (const string &ccypair, bool val) |

| void | setFxVolIsSurface (bool val) |

| void | setFxVolExpiries (const string &name, const vector< Period > &expiries) |

| void | setFxVolDecayMode (const string &val) |

| void | setFxVolCcyPairs (vector< string > names) |

| void | setFxVolMoneyness (const string &ccypair, const vector< Real > &moneyness) |

| void | setFxVolMoneyness (const vector< Real > &moneyness) |

| void | setFxVolStdDevs (const string &ccypair, const vector< Real > &stdDevs) |

| void | setFxVolStdDevs (const vector< Real > &stdDevs) |

| void | setFxVolSmileDynamics (const string &name, const string &smileDynamics) |

| void | setSimulateEquityVols (bool simulate) |

| void | setSimulateEquityVolATMOnly (bool simulateATMOnly) |

| void | setEquityVolIsSurface (const string &name, bool isSurface) |

| void | setEquityVolExpiries (const string &name, const vector< Period > &expiries) |

| void | setEquityVolDecayMode (const string &val) |

| void | setEquityVolNames (vector< string > names) |

| void | setEquityVolMoneyness (const string &name, const vector< Real > &moneyness) |

| void | setEquityVolStandardDevs (const string &name, const vector< Real > &standardDevs) |

| void | setEquityVolSmileDynamics (const string &name, const string &smileDynamics) |

| vector< string > & | additionalScenarioDataIndices () |

| void | setAdditionalScenarioDataIndices (const vector< string > &asdi) |

| vector< string > & | additionalScenarioDataCcys () |

| void | setAdditionalScenarioDataCcys (const vector< string > &ccys) |

| void | setSecuritySpreadsSimulate (bool simulate) |

| void | setSecurities (vector< string > names) |

| void | setRecoveryRates (vector< string > names) |

| void | setCprs (const vector< string > &names) |

| void | setSimulateCprs (bool simulate) |

| bool | simulateCprs () const |

| const vector< string > & | cprs () const |

| void | setSimulateBaseCorrelations (bool simulate) |

| vector< Period > & | baseCorrelationTerms () |

| vector< Real > & | baseCorrelationDetachmentPoints () |

| void | setBaseCorrelationNames (vector< string > names) |

| void | setCpiIndices (vector< string > names) |

| void | setZeroInflationIndices (vector< string > names) |

| void | setZeroInflationTenors (const string &key, const vector< Period > &p) |

| void | setYoyInflationIndices (vector< string > names) |

| void | setYoyInflationTenors (const string &key, const vector< Period > &p) |

| void | setCommodityCurveSimulate (bool simulate) |

| void | setCommodityNames (vector< string > names) |

| void | setCommodityCurves (vector< string > names) |

| void | setCommodityCurveTenors (const std::string &commodityName, const std::vector< QuantLib::Period > &p) |

| void | setCommodityVolSimulate (bool simulate) |

| std::string & | commodityVolDecayMode () |

| void | setCommodityVolNames (vector< string > names) |

| std::vector< QuantLib::Period > & | commodityVolExpiries (const std::string &commodityName) |

| std::vector< QuantLib::Real > & | commodityVolMoneyness (const std::string &commodityName) |

| void | setCommodityVolSmileDynamics (const string &key, const string &smileDynamics) |

| void | setSimulateCorrelations (bool simulate) |

| bool & | correlationIsSurface () |

| vector< Period > & | correlationExpiries () |

| void | setCorrelationPairs (vector< string > names) |

| vector< Real > & | correlationStrikes () |

| void | setNumberOfCreditStates (Size numberOfCreditStates) |

Serialisation | |

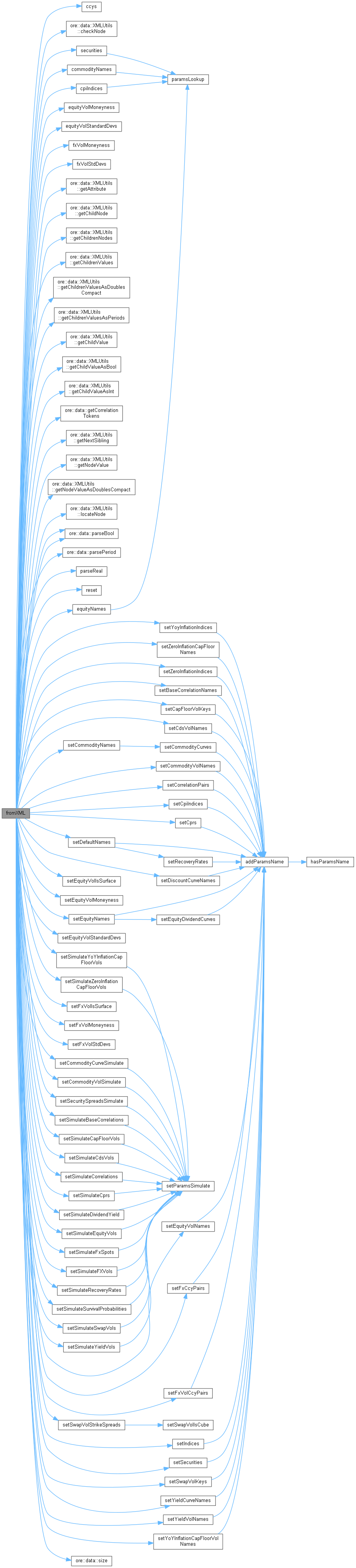

| virtual void | fromXML (XMLNode *node) override |

| virtual XMLNode * | toXML (ore::data::XMLDocument &doc) const override |

| Public Member Functions inherited from XMLSerializable | |

| virtual | ~XMLSerializable () |

| virtual void | fromXML (XMLNode *node)=0 |

| virtual XMLNode * | toXML (XMLDocument &doc) const=0 |

| void | fromFile (const std::string &filename) |

| void | toFile (const std::string &filename) const |

| void | fromXMLString (const std::string &xml) |

| std::string | toXMLString () const |

Equality Operators | |

| string | baseCcy_ |

| vector< string > | ccys_ |

| map< string, string > | yieldCurveCurrencies_ |

| map< string, vector< Period > > | yieldCurveTenors_ |

| map< string, string > | swapIndices_ |

| string | interpolation_ |

| string | extrapolation_ |

| map< string, bool > | swapVolIsCube_ |

| bool | swapVolSimulateATMOnly_ = false |

| map< string, vector< Period > > | swapVolTerms_ |

| map< string, vector< Period > > | swapVolExpiries_ |

| map< string, vector< Real > > | swapVolStrikeSpreads_ |

| string | swapVolDecayMode_ |

| map< string, string > | swapVolSmileDynamics_ |

| vector< Period > | yieldVolTerms_ |

| vector< Period > | yieldVolExpiries_ |

| string | yieldVolDecayMode_ |

| map< string, string > | yieldVolSmileDynamics_ |

| map< string, vector< Period > > | capFloorVolExpiries_ |

| map< std::string, std::vector< QuantLib::Rate > > | capFloorVolStrikes_ |

| map< std::string, bool > | capFloorVolIsAtm_ |

| string | capFloorVolDecayMode_ |

| bool | capFloorVolAdjustOptionletPillars_ |

| bool | capFloorVolUseCapAtm_ |

| map< string, string > | capFloorVolSmileDynamics_ |

| map< string, vector< Period > > | yoyInflationCapFloorVolExpiries_ |

| map< std::string, std::vector< QuantLib::Rate > > | yoyInflationCapFloorVolStrikes_ |

| string | yoyInflationCapFloorVolDecayMode_ |

| map< string, string > | yoyInflationCapFloorVolSmileDynamics_ |

| map< string, vector< Period > > | zeroInflationCapFloorVolExpiries_ |

| map< std::string, std::vector< QuantLib::Rate > > | zeroInflationCapFloorVolStrikes_ |

| string | zeroInflationCapFloorVolDecayMode_ |

| map< string, string > | zeroInflationCapFloorVolSmileDynamics_ |

| map< string, string > | defaultCurveCalendars_ |

| map< string, vector< Period > > | defaultTenors_ |

| string | defaultCurveExtrapolation_ |

| bool | cdsVolSimulateATMOnly_ = false |

| vector< Period > | cdsVolExpiries_ |

| string | cdsVolDecayMode_ |

| map< string, string > | cdsVolSmileDynamics_ |

| map< string, vector< Period > > | equityDividendTenors_ |

| bool | fxVolSimulateATMOnly_ = false |

| map< std::string, bool > | fxVolIsSurface_ |

| map< string, vector< Period > > | fxVolExpiries_ |

| string | fxVolDecayMode_ |

| map< string, vector< Real > > | fxMoneyness_ |

| map< string, vector< Real > > | fxStandardDevs_ |

| map< string, string > | fxVolSmileDynamics_ |

| bool | equityVolSimulateATMOnly_ = false |

| map< string, bool > | equityVolIsSurface_ |

| map< string, vector< Period > > | equityVolExpiries_ |

| string | equityVolDecayMode_ |

| map< string, vector< Real > > | equityMoneyness_ |

| map< string, vector< Real > > | equityStandardDevs_ |

| map< string, string > | equityVolSmileDynamics_ |

| vector< string > | additionalScenarioDataIndices_ |

| vector< string > | additionalScenarioDataCcys_ |

| Size | additionalScenarioDataNumberOfCreditStates_ = 0 |

| vector< string > | additionalScenarioDataSurvivalWeights_ |

| bool | cprSimulate_ |

| vector< string > | cprs_ |

| vector< Period > | baseCorrelationTerms_ |

| vector< Real > | baseCorrelationDetachmentPoints_ |

| map< string, vector< Period > > | zeroInflationTenors_ |

| map< string, vector< Period > > | yoyInflationTenors_ |

| std::map< std::string, std::vector< QuantLib::Period > > | commodityCurveTenors_ |

| std::string | commodityVolDecayMode_ |

| std::map< std::string, std::vector< QuantLib::Period > > | commodityVolExpiries_ |

| std::map< std::string, std::vector< QuantLib::Real > > | commodityVolMoneyness_ |

| map< string, string > | commodityVolSmileDynamics_ |

| bool | correlationIsSurface_ |

| vector< Period > | correlationExpiries_ |

| vector< Real > | correlationStrikes_ |

| Size | numberOfCreditStates_ = 0 |

| std::map< RiskFactorKey::KeyType, std::pair< bool, std::set< std::string > > > | params_ |

| bool | operator== (const ScenarioSimMarketParameters &rhs) |

| bool | operator!= (const ScenarioSimMarketParameters &rhs) |

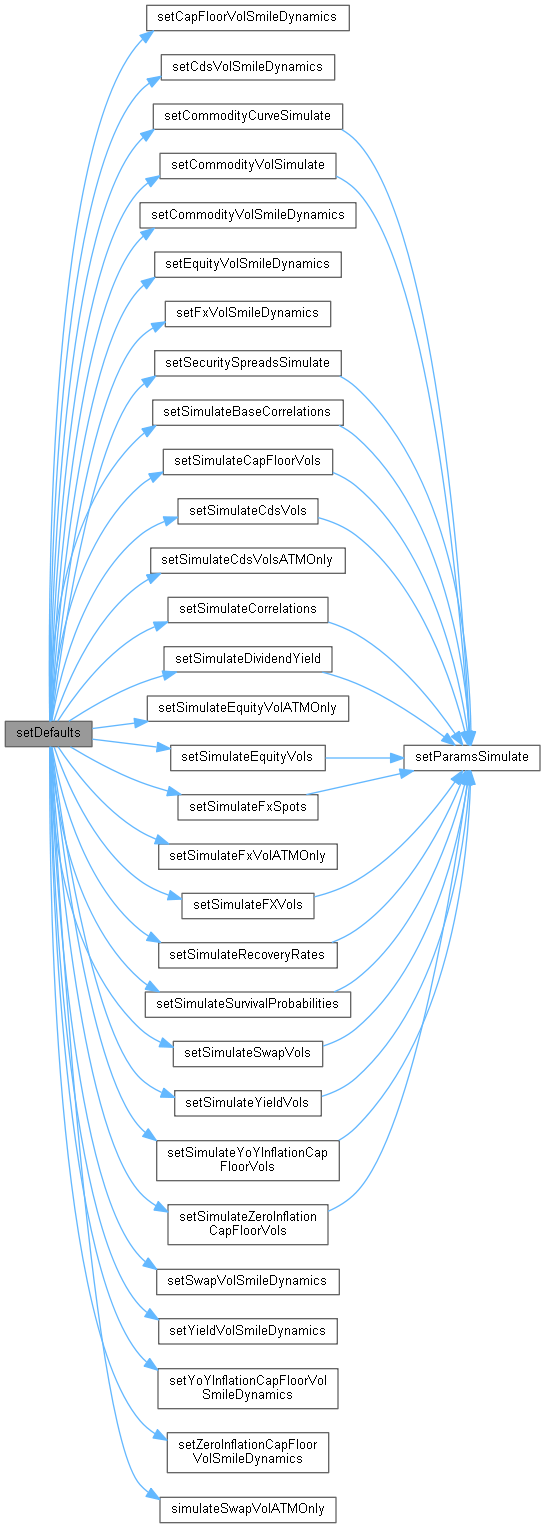

| void | setDefaults () |

| void | reset () |

| A method used to reset the object to its default state before fromXML is called. More... | |

ScenarioSimMarket description.

Definition at line 47 of file scenariosimmarketparameters.hpp.

Default constructor.

Definition at line 50 of file scenariosimmarketparameters.hpp.

| const string & baseCcy | ( | ) | const |

Definition at line 59 of file scenariosimmarketparameters.hpp.

| const vector< string > & ccys | ( | ) | const |

Definition at line 60 of file scenariosimmarketparameters.hpp.

Here is the caller graph for this function:| vector< string > paramsLookup | ( | RiskFactorKey::KeyType | k | ) | const |

Definition at line 62 of file scenariosimmarketparameters.cpp.

Here is the caller graph for this function:| bool hasParamsName | ( | RiskFactorKey::KeyType | kt, |

| string | name | ||

| ) | const |

Definition at line 72 of file scenariosimmarketparameters.cpp.

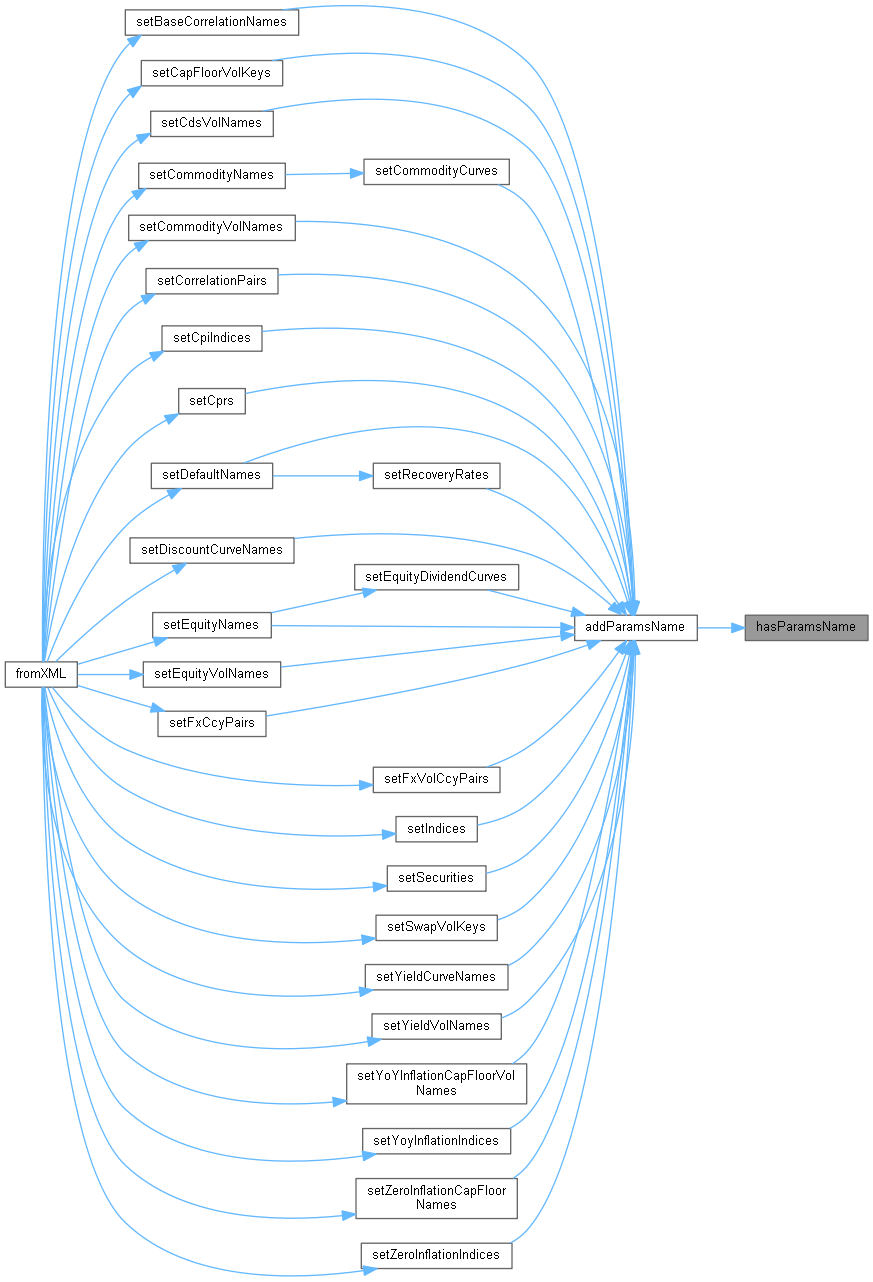

Here is the caller graph for this function:| void addParamsName | ( | RiskFactorKey::KeyType | kt, |

| vector< string > | names | ||

| ) |

Definition at line 81 of file scenariosimmarketparameters.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| bool paramsSimulate | ( | RiskFactorKey::KeyType | kt | ) | const |

Definition at line 94 of file scenariosimmarketparameters.cpp.

Here is the caller graph for this function:| void setParamsSimulate | ( | RiskFactorKey::KeyType | kt, |

| bool | simulate | ||

| ) |

Definition at line 102 of file scenariosimmarketparameters.cpp.

Here is the caller graph for this function:| vector< string > discountCurveNames | ( | ) | const |

Definition at line 67 of file scenariosimmarketparameters.hpp.

Here is the call graph for this function:| vector< string > yieldCurveNames | ( | ) | const |

Definition at line 69 of file scenariosimmarketparameters.hpp.

Here is the call graph for this function: Here is the caller graph for this function:| const map< string, string > & yieldCurveCurrencies | ( | ) | const |

Definition at line 70 of file scenariosimmarketparameters.hpp.

| const vector< Period > & yieldCurveTenors | ( | const string & | key | ) | const |

Definition at line 162 of file scenariosimmarketparameters.cpp.

| bool hasYieldCurveTenors | ( | const string & | key | ) | const |

Definition at line 72 of file scenariosimmarketparameters.hpp.

| vector< string > indices | ( | ) | const |

Definition at line 73 of file scenariosimmarketparameters.hpp.

Here is the call graph for this function: Here is the caller graph for this function:| const map< string, string > & swapIndices | ( | ) | const |

Definition at line 74 of file scenariosimmarketparameters.hpp.

| const string & interpolation | ( | ) | const |

Definition at line 75 of file scenariosimmarketparameters.hpp.

| const string & extrapolation | ( | ) | const |

Definition at line 76 of file scenariosimmarketparameters.hpp.

| const map< string, vector< Period > > & yieldCurveTenors | ( | ) | const |

Definition at line 77 of file scenariosimmarketparameters.hpp.

| bool simulateFxSpots | ( | ) | const |

Definition at line 79 of file scenariosimmarketparameters.hpp.

Here is the call graph for this function:| vector< string > fxCcyPairs | ( | ) | const |

Definition at line 80 of file scenariosimmarketparameters.hpp.

Here is the call graph for this function: Here is the caller graph for this function:| bool simulateSwapVols | ( | ) | const |

Definition at line 82 of file scenariosimmarketparameters.hpp.

Here is the call graph for this function: Here is the caller graph for this function:| bool swapVolIsCube | ( | const string & | key | ) | const |

Definition at line 192 of file scenariosimmarketparameters.cpp.

| bool simulateSwapVolATMOnly | ( | ) | const |

Definition at line 84 of file scenariosimmarketparameters.hpp.

Here is the caller graph for this function:| const vector< Period > & swapVolTerms | ( | const string & | key | ) | const |

Definition at line 222 of file scenariosimmarketparameters.cpp.

| const vector< Period > & swapVolExpiries | ( | const string & | key | ) | const |

Definition at line 226 of file scenariosimmarketparameters.cpp.

| vector< string > swapVolKeys | ( | ) | const |

Definition at line 87 of file scenariosimmarketparameters.hpp.

Here is the call graph for this function: Here is the caller graph for this function:| const string & swapVolDecayMode | ( | ) | const |

Definition at line 88 of file scenariosimmarketparameters.hpp.

| const vector< Real > & swapVolStrikeSpreads | ( | const string & | key | ) | const |

Definition at line 230 of file scenariosimmarketparameters.cpp.

| const string & swapVolSmileDynamics | ( | const string & | key | ) | const |

Definition at line 194 of file scenariosimmarketparameters.cpp.

| bool simulateYieldVols | ( | ) | const |

Definition at line 92 of file scenariosimmarketparameters.hpp.

Here is the call graph for this function: Here is the caller graph for this function:| const vector< Period > & yieldVolTerms | ( | ) | const |

Definition at line 93 of file scenariosimmarketparameters.hpp.

| const vector< Period > & yieldVolExpiries | ( | ) | const |

Definition at line 94 of file scenariosimmarketparameters.hpp.

| vector< string > yieldVolNames | ( | ) | const |

Definition at line 95 of file scenariosimmarketparameters.hpp.

Here is the call graph for this function: Here is the caller graph for this function:| const string & yieldVolDecayMode | ( | ) | const |

Definition at line 96 of file scenariosimmarketparameters.hpp.

| const string & yieldVolSmileDynamics | ( | const string & | key | ) | const |

Definition at line 197 of file scenariosimmarketparameters.cpp.

| bool simulateCapFloorVols | ( | ) | const |

Definition at line 99 of file scenariosimmarketparameters.hpp.

Here is the call graph for this function: Here is the caller graph for this function:| vector< string > capFloorVolKeys | ( | ) | const |

Definition at line 100 of file scenariosimmarketparameters.hpp.

Here is the call graph for this function: Here is the caller graph for this function:| const vector< Period > & capFloorVolExpiries | ( | const string & | key | ) | const |

Definition at line 166 of file scenariosimmarketparameters.cpp.

| bool hasCapFloorVolExpiries | ( | const string & | key | ) | const |

Definition at line 102 of file scenariosimmarketparameters.hpp.

| const vector< Rate > & capFloorVolStrikes | ( | const std::string & | key | ) | const |

Definition at line 170 of file scenariosimmarketparameters.cpp.

| bool capFloorVolIsAtm | ( | const std::string & | key | ) | const |

Definition at line 174 of file scenariosimmarketparameters.cpp.

| const string & capFloorVolDecayMode | ( | ) | const |

Definition at line 105 of file scenariosimmarketparameters.hpp.

| bool capFloorVolAdjustOptionletPillars | ( | ) | const |

If true, the capFloorVolExpiries are interpreted as cap maturities and the pillars for the optionlet structure are set equal to the fixing date of the last optionlet on the cap. If false, the capFloorVolExpiries are the pillars for the optionlet structure.

Definition at line 110 of file scenariosimmarketparameters.hpp.

Here is the caller graph for this function:| bool capFloorVolUseCapAtm | ( | ) | const |

If true, use ATM cap rate when capFloorVolIsAtm is true when querying the todaysmarket optionlet volatility structure at the configured expiries. Otherwise, use the index forward rate.

Definition at line 114 of file scenariosimmarketparameters.hpp.

Here is the caller graph for this function:| const string & capFloorVolSmileDynamics | ( | const string & | key | ) | const |

Definition at line 200 of file scenariosimmarketparameters.cpp.

| bool simulateYoYInflationCapFloorVols | ( | ) | const |

Definition at line 117 of file scenariosimmarketparameters.hpp.

Here is the call graph for this function: Here is the caller graph for this function:| vector< string > yoyInflationCapFloorVolNames | ( | ) | const |

Definition at line 120 of file scenariosimmarketparameters.hpp.

Here is the call graph for this function: Here is the caller graph for this function:| const vector< Period > & yoyInflationCapFloorVolExpiries | ( | const string & | key | ) | const |

Definition at line 176 of file scenariosimmarketparameters.cpp.

| bool hasYoYInflationCapFloorVolExpiries | ( | const string & | key | ) | const |

Definition at line 124 of file scenariosimmarketparameters.hpp.

| const vector< Rate > & yoyInflationCapFloorVolStrikes | ( | const std::string & | key | ) | const |

Definition at line 180 of file scenariosimmarketparameters.cpp.

| const string & yoyInflationCapFloorVolDecayMode | ( | ) | const |

Definition at line 128 of file scenariosimmarketparameters.hpp.

Here is the caller graph for this function:| const string & yoyInflationCapFloorVolSmileDynamics | ( | const string & | key | ) | const |

Definition at line 203 of file scenariosimmarketparameters.cpp.

| bool simulateZeroInflationCapFloorVols | ( | ) | const |

Definition at line 131 of file scenariosimmarketparameters.hpp.

Here is the call graph for this function: Here is the caller graph for this function:| vector< string > zeroInflationCapFloorVolNames | ( | ) | const |

Definition at line 134 of file scenariosimmarketparameters.hpp.

Here is the call graph for this function: Here is the caller graph for this function:| const vector< Period > & zeroInflationCapFloorVolExpiries | ( | const string & | key | ) | const |

Definition at line 234 of file scenariosimmarketparameters.cpp.

| bool hasZeroInflationCapFloorVolExpiries | ( | const string & | key | ) | const |

Definition at line 138 of file scenariosimmarketparameters.hpp.

| const vector< Rate > & zeroInflationCapFloorVolStrikes | ( | const string & | key | ) | const |

Definition at line 238 of file scenariosimmarketparameters.cpp.

| const string & zeroInflationCapFloorVolDecayMode | ( | ) | const |

Definition at line 142 of file scenariosimmarketparameters.hpp.

Here is the caller graph for this function:| const string & zeroInflationCapFloorVolSmileDynamics | ( | const string & | key | ) | const |

Definition at line 206 of file scenariosimmarketparameters.cpp.

| bool simulateSurvivalProbabilities | ( | ) | const |

Definition at line 145 of file scenariosimmarketparameters.hpp.

Here is the call graph for this function: Here is the caller graph for this function:| bool simulateRecoveryRates | ( | ) | const |

Definition at line 146 of file scenariosimmarketparameters.hpp.

Here is the call graph for this function: Here is the caller graph for this function:| vector< string > defaultNames | ( | ) | const |

Definition at line 147 of file scenariosimmarketparameters.hpp.

Here is the call graph for this function: Here is the caller graph for this function:| const string & defaultCurveCalendar | ( | const string & | key | ) | const |

Definition at line 188 of file scenariosimmarketparameters.cpp.

| const vector< Period > & defaultTenors | ( | const string & | key | ) | const |

Definition at line 184 of file scenariosimmarketparameters.cpp.

| bool hasDefaultTenors | ( | const string & | key | ) | const |

Definition at line 150 of file scenariosimmarketparameters.hpp.

| const string & defaultCurveExtrapolation | ( | ) | const |

Definition at line 151 of file scenariosimmarketparameters.hpp.

| bool simulateCdsVols | ( | ) | const |

Definition at line 153 of file scenariosimmarketparameters.hpp.

Here is the call graph for this function: Here is the caller graph for this function:| bool simulateCdsVolATMOnly | ( | ) | const |

Definition at line 154 of file scenariosimmarketparameters.hpp.

| const vector< Period > & cdsVolExpiries | ( | ) | const |

Definition at line 155 of file scenariosimmarketparameters.hpp.

| vector< string > cdsVolNames | ( | ) | const |

Definition at line 156 of file scenariosimmarketparameters.hpp.

Here is the call graph for this function: Here is the caller graph for this function:| const string & cdsVolDecayMode | ( | ) | const |

Definition at line 157 of file scenariosimmarketparameters.hpp.

| const string & cdsVolSmileDynamics | ( | const string & | key | ) | const |

Definition at line 209 of file scenariosimmarketparameters.cpp.

| vector< string > equityNames | ( | ) | const |

Definition at line 160 of file scenariosimmarketparameters.hpp.

Here is the call graph for this function: Here is the caller graph for this function:| const vector< Period > & equityDividendTenors | ( | const string & | key | ) | const |

Definition at line 242 of file scenariosimmarketparameters.cpp.

| bool hasEquityDividendTenors | ( | const string & | key | ) | const |

Definition at line 162 of file scenariosimmarketparameters.hpp.

| vector< string > equityDividendYields | ( | ) | const |

Definition at line 163 of file scenariosimmarketparameters.hpp.

Here is the call graph for this function:| bool simulateDividendYield | ( | ) | const |

Definition at line 164 of file scenariosimmarketparameters.hpp.

Here is the call graph for this function: Here is the caller graph for this function:| bool simulateFXVols | ( | ) | const |

Definition at line 167 of file scenariosimmarketparameters.hpp.

Here is the call graph for this function: Here is the caller graph for this function:| bool simulateFxVolATMOnly | ( | ) | const |

Definition at line 168 of file scenariosimmarketparameters.hpp.

| bool fxVolIsSurface | ( | const std::string & | ccypair | ) | const |

Definition at line 278 of file scenariosimmarketparameters.cpp.

| bool fxUseMoneyness | ( | const std::string & | ccypair | ) | const |

Definition at line 282 of file scenariosimmarketparameters.cpp.

| const vector< Period > & fxVolExpiries | ( | const string & | key | ) | const |

Definition at line 389 of file scenariosimmarketparameters.cpp.

| const string & fxVolDecayMode | ( | ) | const |

Definition at line 172 of file scenariosimmarketparameters.hpp.

| vector< string > fxVolCcyPairs | ( | ) | const |

Definition at line 173 of file scenariosimmarketparameters.hpp.

Here is the call graph for this function: Here is the caller graph for this function:| const vector< Real > & fxVolMoneyness | ( | const string & | ccypair | ) | const |

Definition at line 270 of file scenariosimmarketparameters.cpp.

Here is the caller graph for this function:| const vector< Real > & fxVolStdDevs | ( | const string & | ccypair | ) | const |

Definition at line 274 of file scenariosimmarketparameters.cpp.

Here is the caller graph for this function:| const string & fxVolSmileDynamics | ( | const string & | key | ) | const |

Definition at line 212 of file scenariosimmarketparameters.cpp.

| bool simulateEquityVols | ( | ) | const |

Definition at line 178 of file scenariosimmarketparameters.hpp.

Here is the call graph for this function: Here is the caller graph for this function:| bool simulateEquityVolATMOnly | ( | ) | const |

Definition at line 179 of file scenariosimmarketparameters.hpp.

| bool equityUseMoneyness | ( | const string & | key | ) | const |

Definition at line 628 of file scenariosimmarketparameters.cpp.

| bool equityVolIsSurface | ( | const string & | key | ) | const |

Definition at line 637 of file scenariosimmarketparameters.cpp.

| const vector< Period > & equityVolExpiries | ( | const string & | key | ) | const |

Definition at line 641 of file scenariosimmarketparameters.cpp.

| const string & equityVolDecayMode | ( | ) | const |

Definition at line 183 of file scenariosimmarketparameters.hpp.

| vector< string > equityVolNames | ( | ) | const |

Definition at line 184 of file scenariosimmarketparameters.hpp.

Here is the call graph for this function: Here is the caller graph for this function:| const vector< Real > & equityVolMoneyness | ( | const string & | key | ) | const |

Definition at line 645 of file scenariosimmarketparameters.cpp.

Here is the caller graph for this function:| const vector< Real > & equityVolStandardDevs | ( | const string & | key | ) | const |

Definition at line 649 of file scenariosimmarketparameters.cpp.

Here is the caller graph for this function:| const string & equityVolSmileDynamics | ( | const string & | key | ) | const |

Definition at line 215 of file scenariosimmarketparameters.cpp.

| const vector< string > & additionalScenarioDataIndices | ( | ) | const |

Definition at line 189 of file scenariosimmarketparameters.hpp.

| const vector< string > & additionalScenarioDataCcys | ( | ) | const |

Definition at line 190 of file scenariosimmarketparameters.hpp.

| const Size additionalScenarioDataNumberOfCreditStates | ( | ) | const |

Definition at line 191 of file scenariosimmarketparameters.hpp.

| const vector< string > & additionalScenarioDataSurvivalWeights | ( | ) | const |

Definition at line 192 of file scenariosimmarketparameters.hpp.

| bool securitySpreadsSimulate | ( | ) | const |

Definition at line 194 of file scenariosimmarketparameters.hpp.

Here is the call graph for this function: Here is the caller graph for this function:| vector< string > securities | ( | ) | const |

Definition at line 195 of file scenariosimmarketparameters.hpp.

Here is the call graph for this function: Here is the caller graph for this function:| bool simulateBaseCorrelations | ( | ) | const |

Definition at line 197 of file scenariosimmarketparameters.hpp.

Here is the call graph for this function: Here is the caller graph for this function:| const vector< Period > & baseCorrelationTerms | ( | ) | const |

Definition at line 198 of file scenariosimmarketparameters.hpp.

| const vector< Real > & baseCorrelationDetachmentPoints | ( | ) | const |

Definition at line 199 of file scenariosimmarketparameters.hpp.

| vector< string > baseCorrelationNames | ( | ) | const |

Definition at line 200 of file scenariosimmarketparameters.hpp.

Here is the call graph for this function: Here is the caller graph for this function:| vector< string > cpiIndices | ( | ) | const |

Definition at line 202 of file scenariosimmarketparameters.hpp.

Here is the call graph for this function: Here is the caller graph for this function:| vector< string > zeroInflationIndices | ( | ) | const |

Definition at line 203 of file scenariosimmarketparameters.hpp.

Here is the call graph for this function: Here is the caller graph for this function:| const vector< Period > & zeroInflationTenors | ( | const string & | key | ) | const |

Definition at line 246 of file scenariosimmarketparameters.cpp.

| bool hasZeroInflationTenors | ( | const string & | key | ) | const |

Definition at line 205 of file scenariosimmarketparameters.hpp.

| vector< string > yoyInflationIndices | ( | ) | const |

Definition at line 206 of file scenariosimmarketparameters.hpp.

Here is the call graph for this function: Here is the caller graph for this function:| const vector< Period > & yoyInflationTenors | ( | const string & | key | ) | const |

Definition at line 250 of file scenariosimmarketparameters.cpp.

| bool hasYoyInflationTenors | ( | const string & | key | ) | const |

Definition at line 208 of file scenariosimmarketparameters.hpp.

| bool commodityCurveSimulate | ( | ) | const |

Definition at line 211 of file scenariosimmarketparameters.hpp.

Here is the call graph for this function: Here is the caller graph for this function:| vector< string > commodityNames | ( | ) | const |

Definition at line 254 of file scenariosimmarketparameters.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| const vector< Period > & commodityCurveTenors | ( | const std::string & | commodityName | ) | const |

Definition at line 258 of file scenariosimmarketparameters.cpp.

| bool hasCommodityCurveTenors | ( | const std::string & | commodityName | ) | const |

Definition at line 262 of file scenariosimmarketparameters.cpp.

| bool commodityVolSimulate | ( | ) | const |

Definition at line 217 of file scenariosimmarketparameters.hpp.

Here is the call graph for this function: Here is the caller graph for this function:| const std::string & commodityVolDecayMode | ( | ) | const |

Definition at line 218 of file scenariosimmarketparameters.hpp.

| std::vector< std::string > commodityVolNames | ( | ) | const |

Definition at line 219 of file scenariosimmarketparameters.hpp.

Here is the call graph for this function: Here is the caller graph for this function:| const vector< Period > & commodityVolExpiries | ( | const std::string & | commodityName | ) | const |

Definition at line 266 of file scenariosimmarketparameters.cpp.

| const vector< Real > & commodityVolMoneyness | ( | const std::string & | commodityName | ) | const |

Definition at line 292 of file scenariosimmarketparameters.cpp.

| const string & commodityVolSmileDynamics | ( | const string & | commodityName | ) | const |

Definition at line 218 of file scenariosimmarketparameters.cpp.

| bool simulateCorrelations | ( | ) | const |

Definition at line 226 of file scenariosimmarketparameters.hpp.

Here is the call graph for this function: Here is the caller graph for this function:| bool correlationIsSurface | ( | ) | const |

Definition at line 227 of file scenariosimmarketparameters.hpp.

| const vector< Period > & correlationExpiries | ( | ) | const |

Definition at line 228 of file scenariosimmarketparameters.hpp.

| vector< std::string > correlationPairs | ( | ) | const |

Definition at line 229 of file scenariosimmarketparameters.hpp.

Here is the call graph for this function: Here is the caller graph for this function:| const vector< Real > & correlationStrikes | ( | ) | const |

Definition at line 230 of file scenariosimmarketparameters.hpp.

| Size numberOfCreditStates | ( | ) | const |

Definition at line 232 of file scenariosimmarketparameters.hpp.

Here is the caller graph for this function:| const std::map< RiskFactorKey::KeyType, std::pair< bool, std::set< std::string > > > & parameters | ( | ) | const |

Definition at line 235 of file scenariosimmarketparameters.hpp.

| string & baseCcy | ( | ) |

Definition at line 242 of file scenariosimmarketparameters.hpp.

| vector< string > & ccys | ( | ) |

Definition at line 243 of file scenariosimmarketparameters.hpp.

| void setDiscountCurveNames | ( | vector< string > | names | ) |

Definition at line 421 of file scenariosimmarketparameters.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| void setYieldCurveNames | ( | vector< string > | names | ) |

Definition at line 426 of file scenariosimmarketparameters.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| map< string, string > & yieldCurveCurrencies | ( | ) |

Definition at line 246 of file scenariosimmarketparameters.hpp.

| void setYieldCurveTenors | ( | const string & | key, |

| const vector< Period > & | p | ||

| ) |

Definition at line 300 of file scenariosimmarketparameters.cpp.

| void setIndices | ( | vector< string > | names | ) |

Definition at line 430 of file scenariosimmarketparameters.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| map< string, string > & swapIndices | ( | ) |

Definition at line 249 of file scenariosimmarketparameters.hpp.

| string & interpolation | ( | ) |

Definition at line 250 of file scenariosimmarketparameters.hpp.

| string & extrapolation | ( | ) |

Definition at line 251 of file scenariosimmarketparameters.hpp.

| void setSimulateFxSpots | ( | bool | simulate | ) |

Definition at line 600 of file scenariosimmarketparameters.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| void setFxCcyPairs | ( | vector< string > | names | ) |

Definition at line 434 of file scenariosimmarketparameters.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| void setSimulateSwapVols | ( | bool | simulate | ) |

Definition at line 536 of file scenariosimmarketparameters.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| void setSwapVolIsCube | ( | const string & | key, |

| bool | isCube | ||

| ) |

Definition at line 304 of file scenariosimmarketparameters.cpp.

Here is the caller graph for this function:| bool & simulateSwapVolATMOnly | ( | ) |

Definition at line 258 of file scenariosimmarketparameters.hpp.

| void setSwapVolTerms | ( | const string & | key, |

| const vector< Period > & | p | ||

| ) |

Definition at line 336 of file scenariosimmarketparameters.cpp.

| void setSwapVolKeys | ( | vector< string > | names | ) |

Definition at line 438 of file scenariosimmarketparameters.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| void setSwapVolExpiries | ( | const string & | key, |

| const vector< Period > & | p | ||

| ) |

Definition at line 340 of file scenariosimmarketparameters.cpp.

| void setSwapVolStrikeSpreads | ( | const std::string & | key, |

| const std::vector< QuantLib::Rate > & | strikes | ||

| ) |

Definition at line 344 of file scenariosimmarketparameters.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| string & swapVolDecayMode | ( | ) |

Definition at line 263 of file scenariosimmarketparameters.hpp.

| void setSwapVolSmileDynamics | ( | const string & | key, |

| const string & | smileDynamics | ||

| ) |

Definition at line 306 of file scenariosimmarketparameters.cpp.

Here is the caller graph for this function:| void setSimulateYieldVols | ( | bool | simulate | ) |

Definition at line 540 of file scenariosimmarketparameters.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| vector< Period > & yieldVolTerms | ( | ) |

Definition at line 267 of file scenariosimmarketparameters.hpp.

| void setYieldVolNames | ( | vector< string > | names | ) |

Definition at line 442 of file scenariosimmarketparameters.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| vector< Period > & yieldVolExpiries | ( | ) |

Definition at line 269 of file scenariosimmarketparameters.hpp.

| string & yieldVolDecayMode | ( | ) |

Definition at line 270 of file scenariosimmarketparameters.hpp.

| void setYieldVolSmileDynamics | ( | const string & | key, |

| const string & | smileDynamics | ||

| ) |

Definition at line 315 of file scenariosimmarketparameters.cpp.

Here is the caller graph for this function:| void setSimulateCapFloorVols | ( | bool | simulate | ) |

Definition at line 544 of file scenariosimmarketparameters.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| void setCapFloorVolKeys | ( | vector< string > | names | ) |

Definition at line 446 of file scenariosimmarketparameters.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| void setCapFloorVolExpiries | ( | const string & | key, |

| const vector< Period > & | p | ||

| ) |

Definition at line 350 of file scenariosimmarketparameters.cpp.

| void setCapFloorVolStrikes | ( | const std::string & | key, |

| const std::vector< QuantLib::Rate > & | strikes | ||

| ) |

Definition at line 354 of file scenariosimmarketparameters.cpp.

| void setCapFloorVolIsAtm | ( | const std::string & | key, |

| bool | isAtm | ||

| ) |

Definition at line 360 of file scenariosimmarketparameters.cpp.

| string & capFloorVolDecayMode | ( | ) |

Definition at line 278 of file scenariosimmarketparameters.hpp.

| void setCapFloorVolAdjustOptionletPillars | ( | bool | capFloorVolAdjustOptionletPillars | ) |

Definition at line 279 of file scenariosimmarketparameters.hpp.

Here is the call graph for this function:| void setCapFloorVolUseCapAtm | ( | bool | capFloorVolUseCapAtm | ) |

Definition at line 282 of file scenariosimmarketparameters.hpp.

Here is the call graph for this function:| void setCapFloorVolSmileDynamics | ( | const string & | key, |

| const string & | smileDynamics | ||

| ) |

Definition at line 312 of file scenariosimmarketparameters.cpp.

Here is the caller graph for this function:| void setSimulateYoYInflationCapFloorVols | ( | bool | simulate | ) |

Definition at line 548 of file scenariosimmarketparameters.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| void setYoYInflationCapFloorVolNames | ( | vector< string > | names | ) |

Definition at line 450 of file scenariosimmarketparameters.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| void setYoYInflationCapFloorVolExpiries | ( | const string & | key, |

| const vector< Period > & | p | ||

| ) |

Definition at line 552 of file scenariosimmarketparameters.cpp.

| void setYoYInflationCapFloorVolStrikes | ( | const std::string & | key, |

| const std::vector< QuantLib::Rate > & | strikes | ||

| ) |

Definition at line 556 of file scenariosimmarketparameters.cpp.

| string & yoyInflationCapFloorVolDecayMode | ( | ) |

Definition at line 291 of file scenariosimmarketparameters.hpp.

| void setYoYInflationCapFloorVolSmileDynamics | ( | const string & | key, |

| const string & | smileDynamics | ||

| ) |

Definition at line 322 of file scenariosimmarketparameters.cpp.

Here is the caller graph for this function:| void setSimulateZeroInflationCapFloorVols | ( | bool | simulate | ) |

Definition at line 560 of file scenariosimmarketparameters.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| void setZeroInflationCapFloorNames | ( | vector< string > | names | ) |

Definition at line 454 of file scenariosimmarketparameters.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| void setZeroInflationCapFloorVolExpiries | ( | const string & | key, |

| const vector< Period > & | p | ||

| ) |

Definition at line 458 of file scenariosimmarketparameters.cpp.

| void setZeroInflationCapFloorVolStrikes | ( | const std::string & | key, |

| const std::vector< QuantLib::Rate > & | strikes | ||

| ) |

Definition at line 462 of file scenariosimmarketparameters.cpp.

| string & zeroInflationCapFloorVolDecayMode | ( | ) |

Definition at line 298 of file scenariosimmarketparameters.hpp.

| void setZeroInflationCapFloorVolSmileDynamics | ( | const string & | key, |

| const string & | smileDynamics | ||

| ) |

Definition at line 318 of file scenariosimmarketparameters.cpp.

Here is the caller graph for this function:| void setSimulateSurvivalProbabilities | ( | bool | simulate | ) |

Definition at line 564 of file scenariosimmarketparameters.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| void setSimulateRecoveryRates | ( | bool | simulate | ) |

Definition at line 568 of file scenariosimmarketparameters.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| void setDefaultNames | ( | vector< string > | names | ) |

Definition at line 466 of file scenariosimmarketparameters.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| void setDefaultTenors | ( | const string & | key, |

| const vector< Period > & | p | ||

| ) |

Definition at line 369 of file scenariosimmarketparameters.cpp.

| void setDefaultCurveCalendars | ( | const string & | key, |

| const string & | p | ||

| ) |

Definition at line 373 of file scenariosimmarketparameters.cpp.

| void setDefaultCurveExtrapolation | ( | const std::string & | e | ) |

Definition at line 306 of file scenariosimmarketparameters.hpp.

| void setSimulateCdsVols | ( | bool | simulate | ) |

Definition at line 572 of file scenariosimmarketparameters.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| void setSimulateCdsVolsATMOnly | ( | bool | simulateATMOnly | ) |

Definition at line 309 of file scenariosimmarketparameters.hpp.

Here is the caller graph for this function:| vector< Period > & cdsVolExpiries | ( | ) |

Definition at line 310 of file scenariosimmarketparameters.hpp.

| void setCdsVolNames | ( | vector< string > | names | ) |

Definition at line 471 of file scenariosimmarketparameters.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| string & cdsVolDecayMode | ( | ) |

Definition at line 312 of file scenariosimmarketparameters.hpp.

| void setCdsVolSmileDynamics | ( | const string & | key, |

| const string & | smileDynamics | ||

| ) |

Definition at line 309 of file scenariosimmarketparameters.cpp.

Here is the caller graph for this function:| void setEquityNames | ( | vector< string > | names | ) |

Definition at line 475 of file scenariosimmarketparameters.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| void setEquityDividendCurves | ( | vector< string > | names | ) |

Definition at line 480 of file scenariosimmarketparameters.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| void setEquityDividendTenors | ( | const string & | key, |

| const vector< Period > & | p | ||

| ) |

Definition at line 377 of file scenariosimmarketparameters.cpp.

| void setSimulateDividendYield | ( | bool | simulate | ) |

Definition at line 532 of file scenariosimmarketparameters.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| void setSimulateFXVols | ( | bool | simulate | ) |

Definition at line 576 of file scenariosimmarketparameters.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| void setSimulateFxVolATMOnly | ( | bool | simulateATMOnly | ) |

Definition at line 322 of file scenariosimmarketparameters.hpp.

Here is the caller graph for this function:| void setFxVolIsSurface | ( | const string & | ccypair, |

| bool | val | ||

| ) |

Definition at line 393 of file scenariosimmarketparameters.cpp.

Here is the caller graph for this function:| void setFxVolIsSurface | ( | bool | val | ) |

Definition at line 395 of file scenariosimmarketparameters.cpp.

| void setFxVolExpiries | ( | const string & | name, |

| const vector< Period > & | expiries | ||

| ) |

Definition at line 397 of file scenariosimmarketparameters.cpp.

| void setFxVolDecayMode | ( | const string & | val | ) |

Definition at line 401 of file scenariosimmarketparameters.cpp.

| void setFxVolCcyPairs | ( | vector< string > | names | ) |

Definition at line 484 of file scenariosimmarketparameters.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| void setFxVolMoneyness | ( | const string & | ccypair, |

| const vector< Real > & | moneyness | ||

| ) |

Definition at line 403 of file scenariosimmarketparameters.cpp.

Here is the caller graph for this function:| void setFxVolMoneyness | ( | const vector< Real > & | moneyness | ) |

Definition at line 407 of file scenariosimmarketparameters.cpp.

| void setFxVolStdDevs | ( | const string & | ccypair, |

| const vector< Real > & | stdDevs | ||

| ) |

Definition at line 409 of file scenariosimmarketparameters.cpp.

Here is the caller graph for this function:| void setFxVolStdDevs | ( | const vector< Real > & | stdDevs | ) |

Definition at line 413 of file scenariosimmarketparameters.cpp.

| void setFxVolSmileDynamics | ( | const string & | name, |

| const string & | smileDynamics | ||

| ) |

Definition at line 329 of file scenariosimmarketparameters.cpp.

Here is the caller graph for this function:| void setSimulateEquityVols | ( | bool | simulate | ) |

Definition at line 580 of file scenariosimmarketparameters.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| void setSimulateEquityVolATMOnly | ( | bool | simulateATMOnly | ) |

Definition at line 335 of file scenariosimmarketparameters.hpp.

Here is the caller graph for this function:| void setEquityVolIsSurface | ( | const string & | name, |

| bool | isSurface | ||

| ) |

Definition at line 612 of file scenariosimmarketparameters.cpp.

Here is the caller graph for this function:| void setEquityVolExpiries | ( | const string & | name, |

| const vector< Period > & | expiries | ||

| ) |

Definition at line 616 of file scenariosimmarketparameters.cpp.

| void setEquityVolDecayMode | ( | const string & | val | ) |

Definition at line 338 of file scenariosimmarketparameters.hpp.

| void setEquityVolNames | ( | vector< string > | names | ) |

Definition at line 488 of file scenariosimmarketparameters.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| void setEquityVolMoneyness | ( | const string & | name, |

| const vector< Real > & | moneyness | ||

| ) |

Definition at line 620 of file scenariosimmarketparameters.cpp.

Here is the caller graph for this function:| void setEquityVolStandardDevs | ( | const string & | name, |

| const vector< Real > & | standardDevs | ||

| ) |

Definition at line 624 of file scenariosimmarketparameters.cpp.

Here is the caller graph for this function:| void setEquityVolSmileDynamics | ( | const string & | name, |

| const string & | smileDynamics | ||

| ) |

Definition at line 326 of file scenariosimmarketparameters.cpp.

Here is the caller graph for this function:| vector< string > & additionalScenarioDataIndices | ( | ) |

Definition at line 344 of file scenariosimmarketparameters.hpp.

| void setAdditionalScenarioDataIndices | ( | const vector< string > & | asdi | ) |

Definition at line 345 of file scenariosimmarketparameters.hpp.

| vector< string > & additionalScenarioDataCcys | ( | ) |

Definition at line 346 of file scenariosimmarketparameters.hpp.

| void setAdditionalScenarioDataCcys | ( | const vector< string > & | ccys | ) |

Definition at line 347 of file scenariosimmarketparameters.hpp.

Here is the call graph for this function:| void setSecuritySpreadsSimulate | ( | bool | simulate | ) |

Definition at line 596 of file scenariosimmarketparameters.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| void setSecurities | ( | vector< string > | names | ) |

Definition at line 492 of file scenariosimmarketparameters.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| void setRecoveryRates | ( | vector< string > | names | ) |

Definition at line 496 of file scenariosimmarketparameters.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| void setCprs | ( | const vector< string > & | names | ) |

Definition at line 528 of file scenariosimmarketparameters.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| void setSimulateCprs | ( | bool | simulate | ) |

Definition at line 608 of file scenariosimmarketparameters.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| bool simulateCprs | ( | ) | const |

Definition at line 354 of file scenariosimmarketparameters.hpp.

Here is the call graph for this function: Here is the caller graph for this function:| const vector< string > & cprs | ( | ) | const |

Definition at line 355 of file scenariosimmarketparameters.hpp.

Here is the caller graph for this function:| void setSimulateBaseCorrelations | ( | bool | simulate | ) |

Definition at line 584 of file scenariosimmarketparameters.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| vector< Period > & baseCorrelationTerms | ( | ) |

Definition at line 358 of file scenariosimmarketparameters.hpp.

| vector< Real > & baseCorrelationDetachmentPoints | ( | ) |

Definition at line 359 of file scenariosimmarketparameters.hpp.

| void setBaseCorrelationNames | ( | vector< string > | names | ) |

Definition at line 500 of file scenariosimmarketparameters.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| void setCpiIndices | ( | vector< string > | names | ) |

Definition at line 504 of file scenariosimmarketparameters.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| void setZeroInflationIndices | ( | vector< string > | names | ) |

Definition at line 508 of file scenariosimmarketparameters.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| void setZeroInflationTenors | ( | const string & | key, |

| const vector< Period > & | p | ||

| ) |

Definition at line 381 of file scenariosimmarketparameters.cpp.

| void setYoyInflationIndices | ( | vector< string > | names | ) |

Definition at line 512 of file scenariosimmarketparameters.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| void setYoyInflationTenors | ( | const string & | key, |

| const vector< Period > & | p | ||

| ) |

Definition at line 385 of file scenariosimmarketparameters.cpp.

| void setCommodityCurveSimulate | ( | bool | simulate | ) |

Definition at line 588 of file scenariosimmarketparameters.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| void setCommodityNames | ( | vector< string > | names | ) |

Definition at line 415 of file scenariosimmarketparameters.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| void setCommodityCurves | ( | vector< string > | names | ) |

Definition at line 520 of file scenariosimmarketparameters.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| void setCommodityCurveTenors | ( | const std::string & | commodityName, |

| const std::vector< QuantLib::Period > & | p | ||

| ) |

Definition at line 417 of file scenariosimmarketparameters.cpp.

| void setCommodityVolSimulate | ( | bool | simulate | ) |

Definition at line 592 of file scenariosimmarketparameters.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| std::string & commodityVolDecayMode | ( | ) |

Definition at line 376 of file scenariosimmarketparameters.hpp.

| void setCommodityVolNames | ( | vector< string > | names | ) |

Definition at line 516 of file scenariosimmarketparameters.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| std::vector< QuantLib::Period > & commodityVolExpiries | ( | const std::string & | commodityName | ) |

Definition at line 378 of file scenariosimmarketparameters.hpp.

| std::vector< QuantLib::Real > & commodityVolMoneyness | ( | const std::string & | commodityName | ) |

Definition at line 381 of file scenariosimmarketparameters.hpp.

| void setCommodityVolSmileDynamics | ( | const string & | key, |

| const string & | smileDynamics | ||

| ) |

Definition at line 332 of file scenariosimmarketparameters.cpp.

Here is the caller graph for this function:| void setSimulateCorrelations | ( | bool | simulate | ) |

Definition at line 604 of file scenariosimmarketparameters.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| bool & correlationIsSurface | ( | ) |

Definition at line 387 of file scenariosimmarketparameters.hpp.

| vector< Period > & correlationExpiries | ( | ) |

Definition at line 388 of file scenariosimmarketparameters.hpp.

| void setCorrelationPairs | ( | vector< string > | names | ) |

Definition at line 524 of file scenariosimmarketparameters.cpp.

Here is the call graph for this function: Here is the caller graph for this function:| vector< Real > & correlationStrikes | ( | ) |

Definition at line 390 of file scenariosimmarketparameters.hpp.

| void setNumberOfCreditStates | ( | Size | numberOfCreditStates | ) |

Definition at line 391 of file scenariosimmarketparameters.hpp.

Here is the call graph for this function:

|

overridevirtual |

Implements XMLSerializable.

Definition at line 696 of file scenariosimmarketparameters.cpp.

Here is the call graph for this function:

|

overridevirtual |

Implements XMLSerializable.

Definition at line 1547 of file scenariosimmarketparameters.cpp.

Here is the call graph for this function:| bool operator== | ( | const ScenarioSimMarketParameters & | rhs | ) |

Definition at line 653 of file scenariosimmarketparameters.cpp.

| bool operator!= | ( | const ScenarioSimMarketParameters & | rhs | ) |

Definition at line 694 of file scenariosimmarketparameters.cpp.

|

private |

Definition at line 106 of file scenariosimmarketparameters.cpp.

Here is the call graph for this function:

|

private |

A method used to reset the object to its default state before fromXML is called.

Definition at line 157 of file scenariosimmarketparameters.cpp.

Here is the caller graph for this function:

|

private |

Definition at line 412 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 413 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 414 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 415 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 416 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 417 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 418 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 420 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 421 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 422 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 423 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 424 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 425 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 426 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 428 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 429 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 430 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 431 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 433 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 434 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 435 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 436 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 437 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 438 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 439 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 441 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 442 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 443 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 444 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 446 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 447 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 448 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 449 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 451 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 452 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 453 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 455 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 456 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 457 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 458 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 460 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 463 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 464 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 465 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 466 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 467 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 468 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 469 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 471 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 472 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 473 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 474 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 475 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 476 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 477 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 479 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 480 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 481 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 482 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 484 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 485 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 487 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 488 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 490 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 491 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 494 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 497 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 498 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 499 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 500 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 502 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 503 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 504 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 505 of file scenariosimmarketparameters.hpp.

|

private |

Definition at line 509 of file scenariosimmarketparameters.hpp.